A good credit score is one of the most powerful tools in your financial life. It affects everything from whether you can buy a home to the interest rates you’ll pay on loans, and in some cases, even your ability to rent an apartment or land a job. Despite how important it is, many people don’t fully understand how credit scores work, the differences between various credit scoring systems, or what steps they can take to improve them.

In this guide, we’ll explore what credit scores are, the types of credit reporting agencies, how FICO scores differ from others, where to check your scores, and proven strategies to improve them.

What Are Credit Scores?

A credit score is a three-digit number, usually ranging from 300 to 850, that represents your creditworthiness. In simple terms, it’s a financial “grade” that lenders use to decide whether they should give you credit, how much, and at what interest rate.

Credit scores are calculated based on data from your credit report, which includes your borrowing history, repayment habits, outstanding debts, and the length of time you’ve managed credit. A higher score indicates to lenders that you are a responsible borrower, while a lower score suggests greater risk.

Here’s a general breakdown of credit score ranges:

- 300–579: Poor – Approval chances are low, and you may face very high interest rates.

- 580–669: Fair – Some lenders will approve you, but at less favorable terms.

- 670–739: Good – Considered a reliable borrower by most lenders.

- 740–799: Very Good – Eligible for better rates and higher credit limits.

- 800–850: Excellent – The best rates, premium cards, and easy approvals.

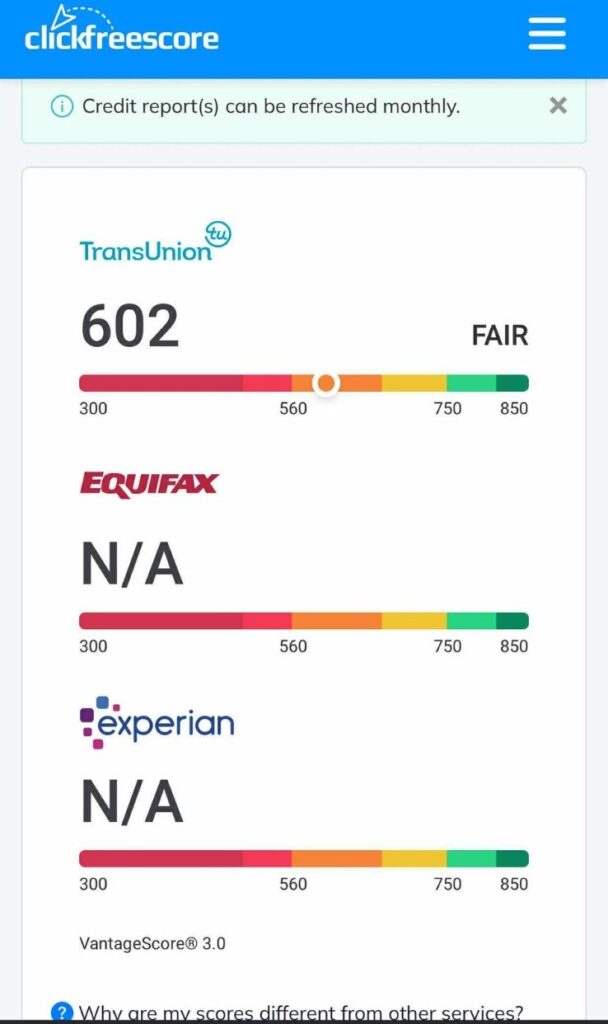

Major Credit Bureaus: TransUnion, Experian, and Equifax

In the United States, three main credit reporting agencies collect your financial data: TransUnion, Experian, and Equifax. Each of them gathers information from banks, credit card companies, and lenders, then compiles it into your credit report.

- TransUnion

- Known for providing detailed consumer credit reports and fraud protection services.

- Offers tools like credit monitoring, alerts, and identity theft protection.

- Their reports often include personal insights into what’s affecting your score.

- Experian

- Offers both personal and business credit reports.

- Allows consumers to use Experian Boost, a tool that adds on-time utility and phone payments to your report to potentially raise your score.

- Provides FICO scores alongside credit reports.

- Equifax

- Another major bureau that collects and sells consumer credit data.

- Offers features like credit freezes, which can prevent identity theft.

- Gained attention in 2017 after a data breach but continues to be a major player in the industry.

⚠️ Important Note: Your credit report may differ slightly between these bureaus because not all lenders report to all three agencies. That’s why your credit score can vary depending on which bureau is checked.

What is BBB and FICO Score?

Better Business Bureau (BBB)

The Better Business Bureau (BBB) is often confused with credit scoring agencies, but it does not deal with personal credit scores. Instead, BBB rates businesses on a scale from A+ to F, based on trustworthiness, complaint history, and transparency. For consumers, checking a financial company’s BBB rating can help determine if they are dealing with a reputable lender or service provider.

FICO Score

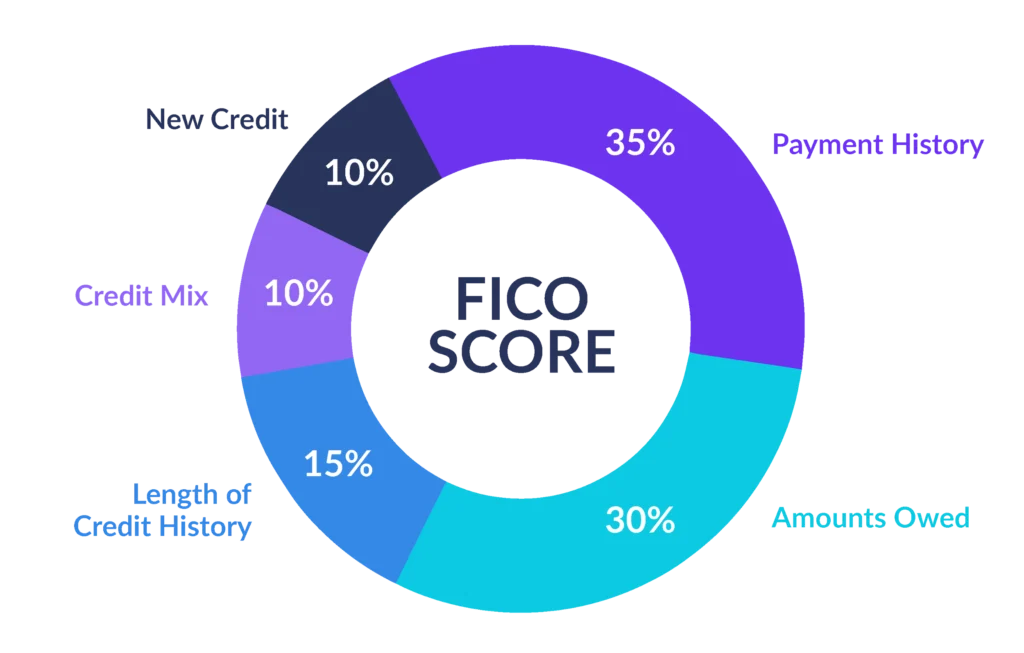

The FICO Score, created by the Fair Isaac Corporation, is the most widely used credit score in the U.S. It uses data from the three bureaus but applies its own formula. Your FICO score is based on five key factors:

- Payment History (35%) – Whether you pay bills on time.

- Credit Utilization (30%) – The percentage of credit you’re using compared to your limit.

- Length of Credit History (15%) – How long you’ve had credit accounts.

- Credit Mix (10%) – A variety of accounts (credit cards, loans, mortgages) helps.

- New Credit Inquiries (10%) – Too many recent applications can lower your score.

FICO Score Ranges:

- 800–850: Exceptional

- 740–799: Very Good

- 670–739: Good

- 580–669: Fair

- Below 580: Poor

How FICO Scores Differ from Credit Bureau Scores

While TransUnion, Experian, and Equifax each generate their own versions of credit scores, FICO scores are the standard most lenders rely on. Here’s the difference:

- Credit Bureau Scores (a.k.a. VantageScore): Each bureau may use its own scoring model, leading to variations in your scores.

- FICO Score: Uses bureau data but applies a uniform formula trusted by 90% of lenders in the U.S.

For example:

- Your Experian score might be 705,

- Your Equifax score could be 715,

- But your FICO score (based on the same data) may calculate to 690.

This is why checking your FICO score in addition to bureau scores is crucial.

How to Improve Your Credit Score

Improving your credit score takes patience, but every step makes a difference. Here’s a detailed guide:

- Pay Bills on Time – Even a single missed payment can drop your score significantly. Set up autopay or reminders.

- Lower Your Credit Utilization – Aim to keep balances below 30% of your credit limit. For the best results, target under 10%.

- Don’t Close Old Accounts – Length of history matters, so keep old cards open even if you don’t use them often.

- Diversify Your Credit Mix – Having both revolving credit (credit cards) and installment loans (car loans, mortgages) strengthens your profile.

- Limit Hard Inquiries – Avoid applying for multiple loans or credit cards in a short period.

- Dispute Errors – Regularly review your credit reports for inaccuracies and file disputes with the bureaus if needed.

Where to Check Your Credit Score

You don’t have to pay for your credit score—there are several free and paid sources.

- View Free Score – The only federally authorized website to get free credit reports from Equifax, Experian, and TransUnion.

- Bureau Websites:

- Credit Monitoring Platforms:

- Credit Karma – Free reports and scores from TransUnion & Equifax.

- Credit Sesame – Free score and monitoring.

- WalletHub – Free daily credit score updates.

- Discover Free Credit Score – Free FICO score for anyone.

- Banks & Credit Cards: Many issuers (Chase, Capital One, Citi, etc.) provide free score tracking in their apps.

How to Check Your Credit Score Step-by-Step

- Visit a trusted credit monitoring site.

- Enter your personal details (name, address, SSN).

- Answer a few identity verification questions.

- Select the bureau(s) you want a report from.

- View your credit score and report instantly.

- Download a copy to review for errors or suspicious activity.

Final Thoughts

Credit scores may seem complicated, but once you understand the basics, managing them becomes much easier. Your credit report is like your financial reputation—it reflects your borrowing habits, discipline, and reliability. By consistently paying bills on time, keeping debt low, and monitoring your reports, you can steadily climb toward an excellent score.

Remember, knowledge is power. The more you understand how credit works, the more control you’ll have over your financial future.

👉 Ready to take the next step? Discover exclusive financial tools, credit improvement offers, and discounts from top brands on our promotions page.